CAL FIRE reminds people that burning is SUSPENDED in all areas.

A Red Flag Warning remains in effect over the eastern Sierra from Lassen County in the north down to Mono County in the south due to gusty winds and low humidity bringing critical fire weather conditions to the area.

In California, there are currently 27 major wildfires/complexes of over 100 acres. As of September 17th, there have been 7,910 fires resulting in approximately 3.5 million total acres burned in 2020.

While a low-pressure system brings slightly cooler temperatures and scattered, unmeasurable precipitation, fire danger remains extreme. A slight amount of rain does not saturate the extremely dry vegetation enough to make any type of burning safe.

Illegal debris burning can result in a citation or worse, a life-threatening wildfire. Now is not the time to burn.

El Dorado County’s Public Health Officer, Dr. Nancy Williams, today announced the County has moved within the State’s new COVID-19 framework for reopening from the Red tier into the less restrictive Orange tier, effective immediately.

“Governor Newsom today officially moved El Dorado County into the Orange tier based on our case rate and

test positivity percentage, allowing many businesses to reopen for the first time since March and others to expand their operations, which is very good news for our economy,” said Williams. “However, as I have stated before, just because something is allowed does not necessarily make it safe.”

Williams said that even though more business sectors are expanding and activities are open, the best way to prevent the County from regressing to the Red tier remains doing the very things that moved the County to the Orange tier.

“Moving to the Orange tier should not be seen as a green light to stop wearing a face covering, keeping at least six feet from others, minimizing mixing with non-household members and washing your hands regularly,” Williams said. “It’s critical, with this positive move forward, to continue to exercise our personal responsibility to ensure we keep our case level and test positivity rate low.”

A county moves into the Orange tier if it has a case rate less than 4.0 per 100,000 residents and a test positivity of less than 5.0. The State records El Dorado County’s population as 193,098. For the most recent week that was assessed, El Dorado County had a 1.5 per 100,000 case rate and 1.4% test positivity.

The most recently calculated test positivity is in the least restrictive Yellow tier, but counties are assigned to the most restrictive tier if its metrics fall into more than one tier.

“As positive as this news is, it requires our continued efforts to stay in the Orange tier and move toward Yellow,” Williams said. “I urge everyone to consider this expansion into the Orange tier as allowing the option to do more, but not necessarily a requirement to do so. Even in the Orange tier, we still need to take the same personal precautions we have been to keep our County healthy.”

El Dorado County’s Registrar of Voters, Bill O’Neill, today announced the timing for when ballots will be mailed to County registered voters and the options voters will have for voting their ballot in the November 2020 general election.

“There has been significant news and concern about the United States Postal Service’s ability to handle the high volume of mail ballots for this election,” said O’Neill. “To ensure our voters receive their ballot timely and without issue we have worked hard to get our ballots produced and ready early. As a result, ballots will be mailed to all registered voters in El Dorado County on Monday, September 28th.”

O’Neill noted that if a registered voter does not receive a ballot by October 5th, they should contact the County Elections office at (530) 621-7480 or by email at elections@edcgov.us

O’Neill reassured voters the upcoming election is being conducted in the same manner as the March Primary election, providing voters with many options, including the following:

Vote By Mail: You can vote your ballot at home and drop it in the mail, postage paid, drop it at our office, in one of the thirteen County of El Dorado drop boxes, or at one of the 13 Vote Centers opening on October 31. The locations of the drop boxes can be found HERE. The location and times of operation for the vote centers can be found HERE and hours for both are below.

In-Person Voting: There will be 13 Vote Centers open for four days prior to Election Day, starting on October 31st for anyone who would like to vote in person. You can vote at ANY Vote Center location, regardless of where you live in the County. You may bring your ballot and surrender it or just show up and check in to receive a new ballot.

“One of the most common questions I receive is about the safety of the election process, particularly given the several options available to voters,” O’Neill said. “Our office has a strict protocol we follow to protect the rights and votes of each registered voter, including processes that check for multiple ballots being cast by a single voter and verifying signatures on file against the ballots cast.” There will COVID safety protocols in place which may cause delays. If you wish to vote in person, please consider voting early and be prepared for a wait.

“I invite anyone with a concern or interested in the process to visit the Elections department and see this transparent process in action,” O’Neill added.

Update on COVID-19 in El Dorado County as of Friday, September 25, 2020.

-- 234 tests (28,622)

-- 11 cases; (1,109)

4 in EDH; 1 in North County; 4 in Cameron Park/Shingle Springs/Rescue; 2 in Lake Tahoe region

3 aged 0-17, 8 aged 18-49, 0 aged 50-64, 0 aged 65+

-- 223 negative tests (27,513)

-- 2 assumed recoveries (1,021)

-- 1 hospitalizations and 1 ICU (1/1)

-- 1.2% positivity rate

(based on specimen collected between Sept 12-18)

-- no new deaths (4)

-- Orange Tier https://covid19.ca.gov/safer-economy/

http://ow.ly/3qSN50zhCuK

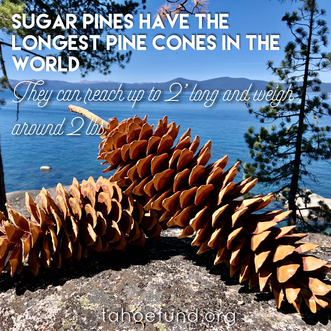

The Sugar Pine produces the longest pine cones in the world, reaching up to two feet long and weighing up to a whopping 2 pounds. Since the 1800's, logging and fire suppression dramatically decreased the sugar pines in the Tahoe Basin. Thanks to your support, the Sugar Pine Foundation and UC - Davis, reforestation of the sugar pines is underway. Watch where you park, pine cones like to fall in the Autumn.

Invitation to Virtual Investigatory Hearing1 on Homeowners' Insurance Availability and Affordability

Insurance Commissioner Ricardo Lara will convene a virtual investigatory hearing2 regarding contemplated changes to the California Code of Regulations to address the pervasive and increasing challenges that homeowners face when seeking and maintaining insurance in high wildfire risk regions of California.

Homeowners’ Insurance Availability and Affordability

California is facing devastating wildfires that are causing unprecedented tragic losses of life and property, mass evacuations, and public health impacts from smoke pollution. Simultaneously, the California Department of Insurance has collected statewide non-renewal data from insurance companies for the past five years, over which time the data demonstrates the same trend: increasing non-renewals for people at risk of wildfires. Climate change is going to continue to displace Californians and disrupt communities through extreme heat and weather. If this trend continues, the ripple effects could impact the entire local economy of communities across the state in the Wildland Urban Interface (WUI) and rural areas, straining families, making home sales more difficult, and negatively impacting the local tax revenues that pay for crucial public health, fire protection, and public safety services, among other adverse impacts.

For the past few decades, California’s insurance companies have been applying for increases to their rates under the existing rate-making process created under Proposition 103, which was passed by voters in November 1988. The Department has analyzed those rate filings and generally approved them, subject to the regulatory review process and consumer protections created under Proposition 103. Yet, even as those rates have been increased, non-renewals have continued. We need to consider options for how to avoid continuing the cycle of wildfires that lead to increased rates but also to address the continued rise in non-renewals across the state while helping ensure the stability of the state’s insurance marketplace. One part of reversing that cycle is to make clear how insurance premiums are established – what factors are included and excluded, and how Californians can help to reduce their risk through investments in wildfire mitigation. Clear incentives for wildfire mitigation are critical to addressing the growing risks of climate change and maintaining a sustainable insurance market.

Today, many insurers voluntarily choose to make sequential rate filings for 6.9% rate increases, rather than make a single filing that is less than the maximum permitted premium that California’s existing regulations

authorize companies to charge under Proposition 103. Insurers who implement this strategy likely do so in order to avoid a mandatory public hearing, should a member of the public petition to intervene in the rate application. Additionally, some homeowners’ insurance companies have chosen to give little to zero weight to proactive home hardening efforts taken by policyholders, instead electing to non-renew policyholders in spite of steps taken to mitigate their homes against the risk of wildfire; conversely, some homeowners’ insurance companies are increasingly choosing to give more weight to homeowners who decide to harden their homes/properties in order to avoid receiving non-renewals.

Administrative Actions are Needed Now - Your Input is Requested

The voters enacted Proposition 103 and vested broad authority in the Commissioner as the regulator of insurance rates. The Commissioner’s authority under Proposition 103 includes broad rulemaking authority to prevent excessive, inadequate, or unfairly discriminatory rates in California. This virtual workshop will provide the public with a deliberate and fair opportunity to discuss issues such as the following:

• Why are insurers declaring their own rates to be ‘inadequate’ and refusing to renew many homes in the wildland-urban interface, while at the same time these same insurers seek rate increases that are lower than California’s law permits?

• Why are insurance companies reluctant to take homeowner wildfire mitigation efforts into account when pricing residential property insurance?

• How will climate change, including extreme heat events, continue to affect future homeowners’ insurance rates, availability of insurance and the financial health of our insurance market?

• How – if at all – would the use of catastrophe modeling in ratemaking help to make homeowners’ insurance more affordable and more widely available to homeowners?

• What other rules should the Commissioner adopt to obligate insurers to spread risk and sell more policies to those homeowners in the wildland-urban interface who seek to purchase and maintain homeowners’ insurance?

You are invited to participate in this investigatory hearing. The purpose of these discussions is to provide interested and affected persons an opportunity to present comments regarding homeowners’ insurance availability and affordability. This forum will serve to foster further conversation as the Commissioner considers administrative actions to address insurance company behavior affecting homeowners in high wildfire risk areas and help homeowners secure and maintain their homeowners’ insurance from the admitted market.

Date, Time, and Format for Workshop

Date: Monday, October 19, 2020

Time: 1:00 p.m. to 5:00 p.m., or as soon after 5:00 p.m. as all those wishing to speak have spoken, whichever is earlier.

Location: Web-based Virtual Format: Details to follow for those who RSVP.

Attendance

To make it possible for the Department to advise attendees of future rulemaking activity and in order to ensure that the web-based format is adequate to accommodate all those who wish to attend, we ask that you please RSVP as soon as possible, but no later than 5:00 p.m. on Monday, October 5, 2020 by providing your name, the name of the organization you represent, and your contact information, including the email address of each attendee, to CDIRegulations@insurance.ca.gov. Doing so will allow the Department to provide a specific on-line invitation so that you may participate. We ask that persons with sight or hearing impairments notify the persons below when they RSVP. Similarly, all interested members of the public should direct inquiries regarding this investigatory hearing to the contact persons named below.

Presentation of Written and Oral Comments

Participants should be prepared to present oral comments on the topics described above and related homeowners’ insurance availability and affordability topics during the public discussions. Participants are also invited to submit written statements and are encouraged to provide supporting documents and materials as well.

This is Not a Formal Public Hearing on Proposed Regulations

Please be advised that participation in this investigatory hearing / workshop will be in addition to, and not in substitution for, any participation in any formal rulemaking process that may follow. This investigatory hearing / workshop invitation does not constitute a Notice of Proposed Action. Consequently, comments (oral or written) received in connection with this hearing will not be included in any record of rulemaking that may follow.

However, any public comments presented will be part of the public record, and the Commissioner will consider all comments received in connection with this hearing as the Commissioner contemplates regulatory changes that may be proposed in a subsequent Notice of Proposed Action.

Contact Persons

All substantive questions and concerns regarding these public discussions should be directed to Lisbeth Landsman-Smith, using the contact information below.

RSVP and Logistical Inquiries

Kathryn Taras, Analyst

California Department of Insurance

300 Capitol Mall, 16th Floor

Sacramento, CA 95814

Phone: (916) 492-3675

Email: CDIRegulations@insurance.ca.gov

Substantive Inquiries

Lisbeth Landsman-Smith

Senior Staff Counsel

California Department of Insurance

300 Capitol Mall, 16th Floor

Sacramento, CA 95814

Phone: (916) 492-3561

Email: Lisbeth.Landsman@insurance.ca.gov

1 This investigatory hearing is held under the authority of Insurance Code section 12924 [investigative powers of Commissioner] and also Government Code section 11346.45 [pre-notice public discussions regarding proposed regulations].

2 Although the Department ordinarily prefers in-person participation, due to unique circumstances during this pandemic, the Department will use a virtual web-conferencing format for this investigatory hearing.

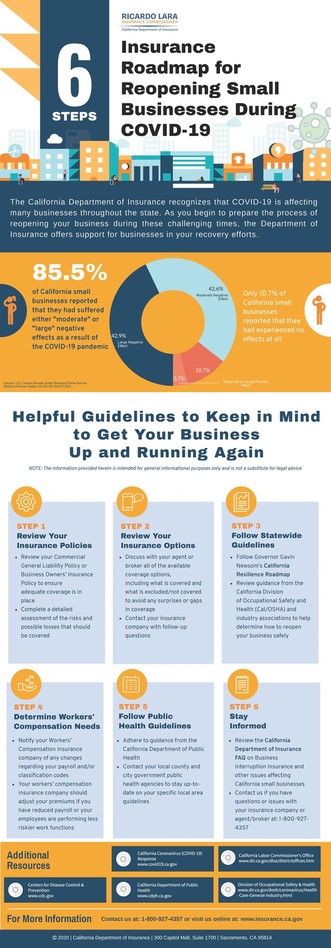

The following is from a letter I received from Insurance Commissioner Ricardo Lara which summarizes the actions taken to further assist survivors, displaced residents, and businesses affected by the current and recent wildfires.

California is facing an unprecedented moment in time battling wildfires throughout the state. I, with the rest of my dedicated staff at the California Department of Insurance, am committed to continuing to serve California consumers during this extraordinary time.

In an effort to further assist survivors, displaced residents, and businesses affected by the current and recent wildfires, and in recognition of Governor Gavin Newsom’s declared state of emergency on August 18, 2020, I have directed the California Department of Insurance (CDI or Department) to take a number of actions with more ahead. Following is an update of recent

wildfire actions that may be helpful to you and your constituents (with more complete details in the full notices):

Continuation of Additional Living Expense (ALE) Benefits Due to Inaccessible/Uninhabitable Homes or Mandatory Evacuations Still in Effect as a Result of Wildfires: On September 3, 2020, I called on all residential property insurance companies to cease terminating ALE benefits while the policyholder’s property remains uninhabitable due to damage caused by the wildfires.

Expedited Claims Handling & Billing Grace Period Procedures for California Policyholders due to Wildfires: On August 26, 2020, I called on all property and casualty insurance companies to implement emergency expedited claims handling procedures and billing grace periods to assist residents and businesses to recover more quickly including:

o Billing Grace Period: All insurers should grant billing leniency for at least 60 days for policyholders in designated wildfire disaster areas.

o Loss of Use, Fair Rental Value or Additional Living Expenses (ALE): Insurers should adopt a standard ALE advance payment of at least 4 months for a total loss. Additional ALE beyond the 4 months should be available upon proper proof following the advance period, upon request of the policyholder.

o Personal Property (Contents): Insurers should provide an initial contents advance payment of at least 25% of policy limits for a total loss of the primary residence in a wildfire disaster without the completion of an inventory. Additional contents payments should be available upon proper proof provided by and upon request of the policyholder.

o Inventory Forms: Insurers should not require that the policyholder use a company-specific inventory form if the policyholder can provide an inventory using a form that contains substantially the same information.

o Inventory Itemization: Insurers should agree to accept an inventory that includes groupings of categories of personal property, including, but not limited to, clothing, shoes, books, food items, CDs, DVDs, or other categories of items for which it would be impractical to separately list each individual item claimed.

o Vehicle Claims: Upon satisfaction of proof of claim, insurers should expedite payment of automobile property damage claims under comprehensive loss

coverage.

o Debris Removal: Insurers should cooperate with a consolidated debris removal process that may be coordinated through city, county, and state agencies, unless the insurer can provide more rapid debris removal outside of the state and local government coordinated effort.

Notice to Insurers of a Forthcoming Bulletin Requiring a Moratorium Against Non-Renewal or Cancellation of Residential Property Insurance Policies for Properties within or Adjacent to a Fire Perimeter Pursuant to Insurance Code Section 675.1(b)(1): On August 26, 2020, I reminded residential property insurers that Insurance Code Section 675.1(b)(1), as enacted by Senate Bill 824 (Lara, Chapter 616, Statutes of 2018), prohibits insurers from non-renewing or cancelling policies of residential property

insurance for residential properties in ZIP Codes within or adjacent to a fire perimeter for one year following a Governor’s declaration of a state of emergency.

Pharmacy Network Adequacy and Prescription Drug Access during U.S. Postal Service Disruptions and Recent States of Emergency Related to Extreme Heat and Wildfires: On August 21, 2020, I reminded insurers of their existing obligations under the Department’s network adequacy regulations and statutory requirements prohibiting restrictions to retail pharmacy access and requiring provision of access to medically necessary health care services during a declared state of emergency.

As always, consumers are encouraged to contact CDI at

1-800-927-4357 or online at http://www.insurance.ca.gov to speak with an expert for help with their questions, concerns, and any claims issues.

|